Business Rehabilitation in Thailand: What Every Thai and Foreign Creditor Needs to Know

As Covid19 continues to wreak havoc around the globe, its devastating impact on Thailand’s economy is becoming increasingly apparent. With its borders closed to international travelers for the foreseeable future, Thailand’s tourism industry, whose revenues account for more than 15% of the country’s total GDP, has been largely decimated. Businesses heavily reliant on tourism have closed their doors in the thousands – and many companies who were already experiencing financial difficulties pre-Covid19 have now been pushed over the edge into insolvency.

Not since the 1997 Asian Financial Crisis has the spotlight been focused so brightly on Thailand’s bankruptcy and business rehabilitation laws – and for good reason. In late April 2020, PACE Development Public Company Limited, one of Thailand’s leading property developers, filed a business rehabilitation petition with Thailand’s Central Bankruptcy Court (the “Court”).

Next came Thailand’s long-embattled national carrier, Thai Airways International Public Company Limited (“THAI”), who filed its own business rehabilitation petition with the Court on May 26, 2020, citing financial difficulties resulting from the Covid19 pandemic. Once seen as a shining corporate beacon and the pride and joy of the nation, the airline is now burdened by debts totaling a staggering THB 354 billion (approximately USD 11.2 billion) as of March 31, 2020. A preliminary hearing is scheduled for August 17, 2020, when the Court will decide whether or not to allow THAI to proceed with its business rehabilitation.

Due to the significance of the Thai Airways case, which is destined to become the largest and possibly most talked about business rehabilitation case in Thailand’s history, and the likelihood that many other business rehabilitations will follow in the coming years, it is not surprising that creditor groups are scrambling to appoint legal counsel in order to protect their interests and to get reacquainted with Thailand’s Bankruptcy Act (the “Bankruptcy Act”), the law which governs Thai bankruptcy and business rehabilitation proceedings.

This newsletter, which is the first in the series on business rehabilitation in Thailand, takes readers through the anatomy of a typical business rehabilitation proceeding under the Bankruptcy Act and highlights a number of the key preliminary issues that both Thai and foreign creditors should be aware of during each stage of the business rehabilitation process.

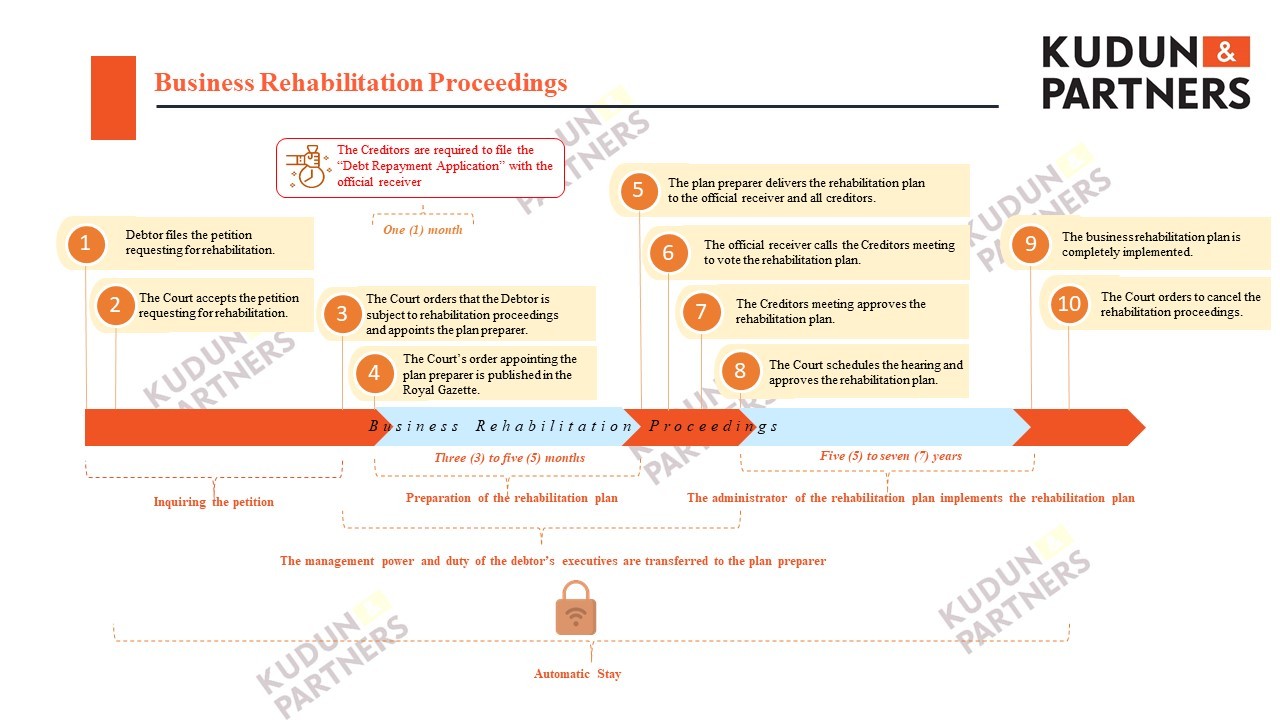

For ease of reference, a diagram illustrating the key milestones and timeframes associated with a typical rehabilitation proceeding in Thailand is shown in Appendix 1 below.

Anatomy Of A Business Rehabilitation Proceeding

The Business Rehabilitation Petition

The business rehabilitation process in Thailand commences when an insolvent debtor, one or group of its creditors, or a competent government authority, files a rehabilitation petition in respect of that debtor with the Court pursuant to Section 90/3 of the Bankruptcy Act (“Rehabilitation Petition”). If the Court accepts the Rehabilitation Petition it will set a hearing date to consider whether or not to allow the debtor to proceed with its rehabilitation and to choose the person or persons who will prepare the rehabilitation plan (the “Preliminary Court Hearing”). Typically, the Preliminary Court Hearing will take place two to three months after the filing of the Rehabilitation Petition. By way of illustration, THAI filed its Rehabilitation Petition with the Court on May 26, 2020, and the Court accepted the THAI’s Rehabilitation Petition on May 27, 2020, setting August 17, 2020, as the date for the Preliminary Court Hearing.

The Automatic Stay

Under Thai law, an automatic stay is an automatic injunction that halts certain actions by the creditors to commence or continue taking action against the debtor or the debtor’s property in order to maintain the debtor’s ordinary business operations during the rehabilitation process. The automatic stay comes into immediate effect the moment the Rehabilitation Petition is accepted by the Court – without the need for any further Court orders – and continues until the Rehabilitation Petition is rejected at the Preliminary Court Hearing or otherwise upon completion or abandonment of the rehabilitation process. Under the Bankruptcy Act, an automatic stay will generally prohibit creditors from filing new claims against the debtor and its assets for repayment of debts, from executing existing judgments against the debtor, or from taking actions to enforce security or other collateral. In addition, while an automatic stay is in effect, creditors are prevented from filing dissolution or bankruptcy proceedings against the debtor.

On the flip side, as a protective measure for creditors, an automatic stay imposes significant restrictions on the ability of the debtor to dispose of, distribute or transfer its assets, to enter into lease arrangements, to repay existing debts or create new debts, or to take actions which have the effect of creating an encumbrance over the debtor’s property, unless necessary for the continuation of the debtor’s normal business operations. Violations of these automatic stay restrictions by a debtor will attract criminal penalties.

Key Considerations for Creditors

Creditors should pay particular attention to the restrictions imposed by the automatic stay provisions of the Bankruptcy Act, particularly in the context of any bilateral debtor discussions, as any agreements entered into with the debtor which are contrary to or inconsistent with these restrictions will not be legally binding on the debtor and may be struck down by the Court as void.

Notwithstanding the foregoing general principles, however, creditors should also be aware that the Court has wide-ranging powers to grant exemptions from the restrictions imposed by the automatic stay provisions of the Bankruptcy Act. Creditors who wish to take actions otherwise restricted by the automatic stay provisions of the Bankruptcy Act should consult your legal counsel to determine whether an application for an exemption could be made to the Court.

The Preliminary Court Hearing

At the Preliminary Court Hearing, the Court will consider two matters: (1) whether to allow the debtor to proceed with its proposed business rehabilitation and (2) the appointment of the person or persons who will prepare the debtor’s rehabilitation plan (the “Plan Preparer”). In deciding whether or not to allow the debtor to proceed with its business rehabilitation, the Court will take into account the matters and apply the legal tests specified in the Bankruptcy Act.

Creditor Objections

Creditors who disagree with the Rehabilitation Petition have the right to challenge it by filing an objection with the Court at least three (3) days before the Preliminary Court Hearing. Typically, creditors might object to a Rehabilitation Petition on the grounds that the debts declared by the debtor are not legitimate, that there are no reasonable grounds cited by the debtor to justify a business rehabilitation, or that the debtor has filed the Rehabilitation Petition in bad faith.

If the Court determines that there are reasonable grounds for reorganizing the debtor’s business and that the debtor has filed the Rehabilitation Petition in good faith, it will issue an order for rehabilitation. However, if the Court determines that there are insufficient grounds to justify a business rehabilitation of the debtor under the Bankruptcy Act, or is of the view that the debtor has filed the Rehabilitation Petition in bad faith, the Court will issue an order to dismiss the Rehabilitation Petition, in which case the automatic stay will immediately cease.

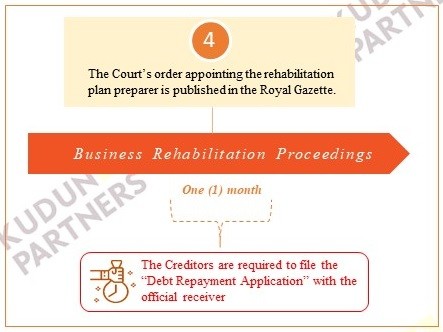

Once the Court issues an order for rehabilitation, the Court will consider the appointment of the Plan Preparer. The Plan Preparer can be the person nominated by the debtor or, if the Court finds such person unsuitable, or if the creditors nominate another person to act as Plan Preparer, a creditors’ meeting will be called to consider the appointment of the Plan Preparer.

The Debt Repayment Application

After the Court issues an order for rehabilitation, creditors must file a debt repayment application (“Debt Repayment Application”) with the Official Receiver within one (1) month from the date that the appointment of the Plan Preparer is published in the Royal Gazette. Creditors should be aware that this one-month period cannot be extended – and the Bankruptcy Act expressly prohibits claims from creditors who fail to file their Debt Repayment Application within the prescribed one-month period.

Key Considerations for Creditors

It is critical that creditors prepare sufficient documentary evidence to support their Debt Repayment Application. Foreign creditors should also be aware that documents in languages other than Thai must be accompanied by certified Thai translations. In addition, any documents supporting a creditor’s Debt Repayment Application made outside Thailand will need to be legalized, notarized or consularized before submission to the Court.

A creditor’s Debt Repayment Application may be challenged by other creditors, the Plan Preparer, and/or the debtor. If this happens, an investigation into the validity of the creditor’s claim will be undertaken and the affected creditor may be required to present additional witnesses and/or evidence in support of its Debt Repayment Application. Upon conclusion of the investigation, the Official Receiver will issue an order specifying the amount of debt owed to such creditor for the purpose of the rehabilitation proceedings – and such amount of debt thereafter be used to calculate the voting rights of the relevant creditor in all creditors’ meetings relating to the rehabilitation proceedings. Accordingly, it is critical that all creditors – particularly foreign creditors to whom additional evidentiary and procedural requirements will apply – must consult Thai legal counsel on their Debt Repayment Application in order to preserve and protect their rights as creditors in the rehabilitation proceedings.

The Business Rehabilitation Plan

The Plan Preparer will commence the preparation of the debtor’s proposed rehabilitation plan (the “Proposed Rehabilitation Plan”) after the Court issues its order for the rehabilitation of the debtor. The Plan Preparer will submit the Proposed Rehabilitation Plan to all creditors and the Official Receiver will call a creditors’ meeting to consider the Proposed Rehabilitation Plan. Pursuant to Section 90/46 of the Bankruptcy Act, the resolution approving the Proposed Rehabilitation Plan must be approved by either:

1. at a meeting of all creditor groups, by a majority vote, provided that the total aggregate debts of the creditors voting in favor of the resolution is not less than two-thirds of the total aggregate debts of all creditors present at the meeting; or

2. at a meeting of one creditor group, by a majority vote, provided that (a) the total aggregate debts of the creditors voting in favor of the resolution is not less than two-thirds of the total aggregate debts of all creditors of that group present at the meeting, and (b) the cumulative amount of debt held by all the creditors who have approved the Proposed Rehabilitation Plan is not less than 50% of the total debt owed by the debtor.

Creditor(s) who disagree with the Proposed Rehabilitation Plan are entitled to propose amendments by filing a petition with the Official Receiver at least three (3) days prior to the date of the creditors’ meeting. If the Proposed Rehabilitation Plan is approved in the creditors’ meeting and endorsed by the Court, a plan administrator will be appointed to implement the approved rehabilitation plan and all creditors will be bound by the repayment terms and conditions specified therein.

Key Considerations for Creditors

Creditors must carefully consider their voting rights and their creditor groupings, as well as any repayment terms and conditions specifically applicable to their creditor group, before casting their vote in the creditors’ meeting.

In the next episode, we will elaborate on the benefits and restrictions of the automatic stay, an overview of the different creditor groups, and the key issues that creditors should insist be included in the Proposed Rehabilitation Plan.

Note: This article examines a typical rehabilitation proceeding in Thailand and is written from a high-level perspective. Please contact us should you have any specific questions regarding your rights as a creditor or debtor in any ongoing or future rehabilitation proceedings in Thailand.

BUSINESS REHABILITATION SPOTLIGHT SERIES EPISODE #2 The Power of the Automatic Stay

BUSINESS REHABILITATION SPOTLIGHT SERIES EPISODE #3 Debt Repayment Application

Appendix 1: Business Rehabilitation Timeline

![]() Download Newsletter

Download Newsletter

Authors:

Pariyapol Kamolsilp

Partner

pariyapol.k@kap.co.th

Troy Schooneman

Partner

troy.s@kap.co.th

Kongwat Akaramanee

Senior Associate

kongwat.a@kap.co.th

Attapon Tanasanti

Associate

attapon.t@kap.co.th

{kind=link}